- From our Sponsors -

The first rule of venture capital is that startups are valued for their growth. But the impact of a company’s revenue growth on shareholder value is often misconstrued. Tom Tunguz explains here why a company’s valuation can decrease even though it is still growing at a healthy rate. He rightly points out that just because a business grows doesn’t means it increases its value. And it certainly doesn’t mean that shareholders who get diluted in the process are better off.

Just because a business grows doesn’t mean that all shareholders are better off.

So how can entrepreneurs and investors assess the impact of revenue growth on the value of their shares and determine whether it is more value accretive to stay the course, raise more capital or sell the company? For that you need to run some numbers. And to make things easier, Venero Capital Advisors prepared a spreadsheet that automates the number crunching. You can download it here and use it.

Below is an example that illustrates the analysis:

Example

You own 30% of a company that generates $5M in revenues. You are evaluating two options:

Option 1: Continue growing the business for another 3 years with the aim to double revenues from $5M to $10M, then look to exit at 5x revenues ($50M deal). To achieve this you need $10M in funding. You receive terms at a $20M pre-money valuation, meaning your stake will be diluted to 20%.

Option 2: Explore an exit today for 5x revenues ($25M valuation).

Important Note: The valuation at which a company fundraises is different than what an acquirer may be willing to pay for the business. Which is why in the Excel you can specify an exit multiple not tied to the company’s funding valuation. Furthermore, this example assumes there are no liquidation preferences, the directional impact of which is shown separately in the Excel model.

So, in this example, which option is more likely to be value accretive? Let’s look at the numbers.

In the Excel, all we have to do is enter our assumptions:

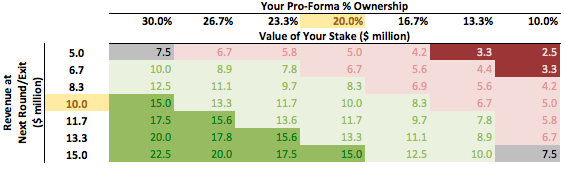

Then look at the outputs. The coloured table and the (6) numbered bullet points shown below are automatically calculated in the Excel:

(1) If you were to exit today at a valuation of 5.0x the current $5.0M revenue, your 30.0% stake would be worth $7.5M.

Not bad.

(2) If you accepted a $10.0M investment at $20.0M valuation and managed to generate $10.0M of revenues within 3 years, your pro-forma 20.0% ownership at 5.0x sales would be worth $10.0M.

So if you accept the investment and increase revenues to $10M, your shares could be worth $2.5M more.

However note that i) your shares would also be worth $10M if you can grow revenues to just $6.7M without investment (and maintain your 30% stake), and ii) this upside comes with significant execution risk, so you should allow margin for error… What if you don’t hit your revenue target?

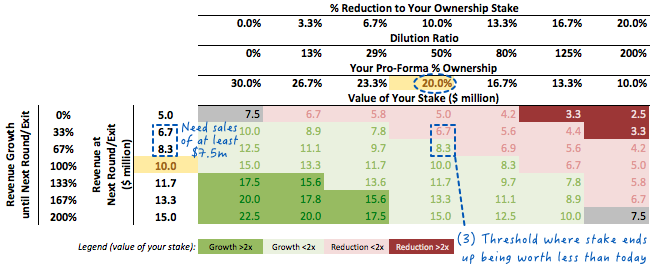

(3) For your stake to not lose value because of the 10.0% dilution (post-money ownership of 20.0%), and assuming you exit 3 years later at 5.0x sales, you will need to increase the current $5.0M revenues by at least $2.5M to $7.5M (50% higher).

If you are comfortable that you will be able to achieve this growth before exiting (or before requiring another round of capital), then consider accepting the investment. In fact, if you believe strongly in the $10M revenue target, there is headroom to accept even greater dilution:

(4) If you believe strongly that in 3 years revenue will be $10.0M then you can afford to reduce your ownership from 30.0% to as little as 15.0% (i.e. accept a $10.0M pre-money valuation) and still be no worse off (but no better off either).

The final aspect to consider is whether the potential upside is worth the execution risk and effort. In this case we assume you want the chance of doubling (2.0x) the value of your shares for it to be worthwhile.

(5) For a dilution of your ownership to 20.0% to be worthwhile (considering all the work you will be putting in and the risk you will be taking with the business over the next 3 years), revenues need to increase from $5.0M to $15.0M (200% growth) so that your pro-forma ownership is worth 2.0x your current stake.

(6) Alternatively, if you don’t believe you can exceed the $10.0M revenue target, you will need a 30.0% ownership in 3 years for it to be worth $15.0M (2.0x today’s value), assuming a 5.0x revenue valuation multiple.

But wait, there’s more…! Bonus Tip: You can quickly determine whether a funding round is likely to be value-accretive by comparing your Dilution Ratio to the company’s projected Growth Rate.

Dilution Ratio = “post-money ownership %” / “pre-money ownership %” - 1.

What about liquidation preferences? Modelling the impact of multiple liquidation preferences can get complicated and is beyond the scope of this analysis, however a separate table in the Excel shows the directional impact. In the above example, a 1.0x liquidation preference means you would get virtually no additional upside if you doubled revenues from $5M to $10M.

That’s it! Try it yourself and let us know if you find the tool useful. Happy number crunching!

PS — If you prefer to value your company e.g. on an EBITDA basis, you can use the Excel in exactly the same way, just replace Revenue with EBITDA throughout.

- From our Sponsors -